How to Avoid Overfitting When Backtesting Strategies

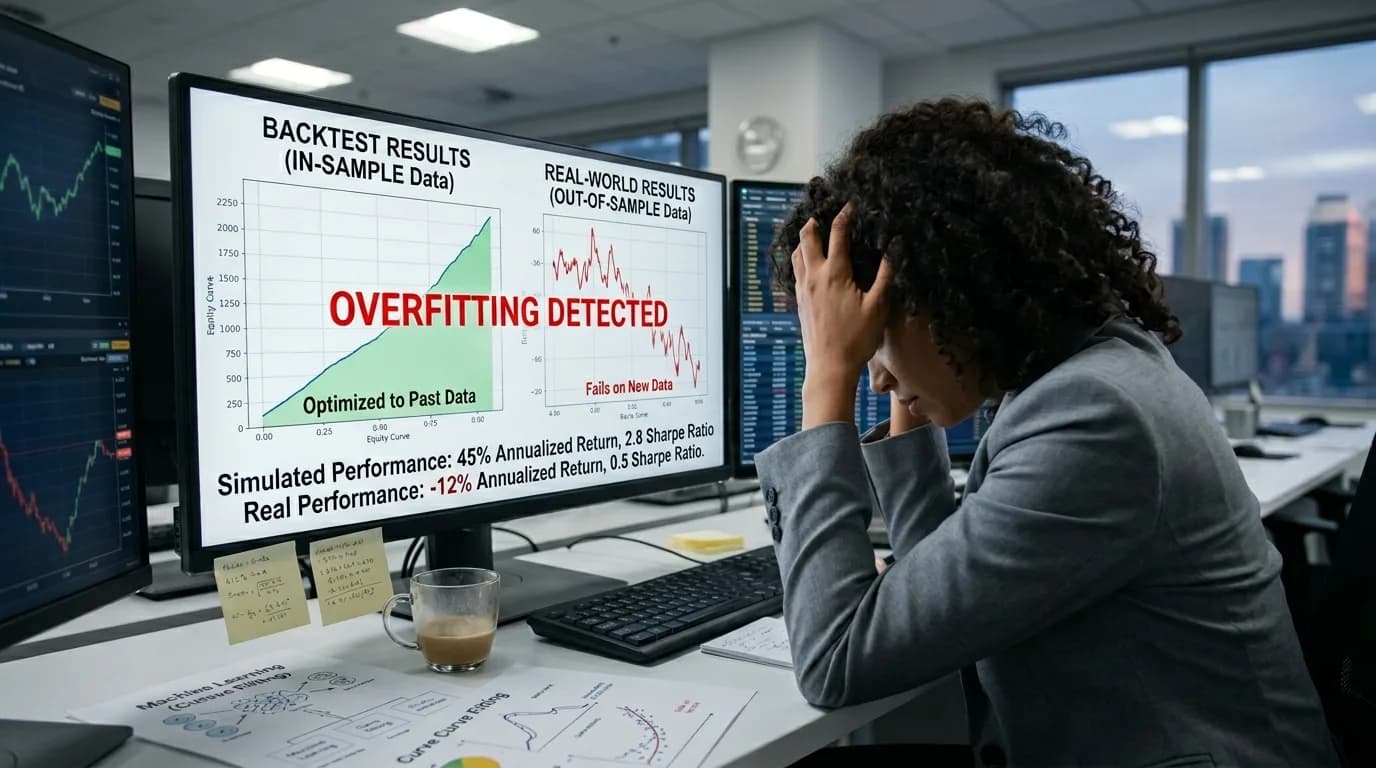

In 2018, I spent three weeks building what I thought was the perfect BTC scalping strategy. RSI divergence confirmation, Bollinger Band squeeze detection, volume filter, session filter, volatility regime filter — the works. Backtest showed 340% annual return with 14% max drawdown. I deployed it live. Within twelve days, I was down 8% with zero winning trades. The strategy was a masterpiece of overfitting, and I'd fooled myself completely.

Overfitting is the most common and most destructive error in strategy development. It's also the most subtle — because the overfitted strategy looks great in your backtest. Perfect, even. That's the trap.

Understanding Overfitting

Every dataset contains two components: signal (genuine, repeating market patterns) and noise (random fluctuations that happened to occur but carry no predictive information). A well-designed strategy captures signal. An overfitted strategy captures noise.

The problem is that noise looks identical to signal in historical data. The only way to distinguish them is to test on data the strategy has never seen. If performance holds up on new data, the patterns are probably real. If it collapses, you were fitting noise.

Think of it like this: if I give you a coin flip sequence — HHTHTTHHHTTH — and ask you to find a pattern, your brain will find one. Maybe "two heads always follow a tail." You could build a model that "predicts" this specific sequence with 80% accuracy. But the sequence was random. Your model works perfectly on this data and fails completely on any new sequence.

The Seven Warning Signs

Here's how to detect overfitting before it costs you money:

| # | Warning Sign | Why It Matters |

|---|---|---|

| 1 | Too many parameters (> 5) | More parameters = more ways to fit noise |

| 2 | Performance drops 50%+ on out-of-sample data | Strategy captured noise, not signal |

| 3 | Very specific parameter values (RSI = 13.7) | Round numbers would work if the pattern is real |

| 4 | Win rate above 80% | Unrealistically high for most strategy types |

| 5 | Works on only one instrument | Pattern is likely data-specific, not market-structural |

| 6 | Small parameter changes destroy performance | Fragile optimization — no robustness zone |

| 7 | Sharpe ratio above 3.0 | Virtually impossible without overfitting or data errors |

The Parameter Sensitivity Test

This is my single favorite anti-overfitting technique. It takes five minutes and catches most overfitting immediately.

Take each parameter in your strategy and vary it by ±20%. If your strategy uses RSI(14), test RSI(11) and RSI(17). If you use EMA(21), test EMA(17) and EMA(25). For every parameter, create a 3x3 or 5x5 grid of combinations.

A robust strategy should show positive expected value across most of the grid. The optimal point might have the highest return, but the surrounding points should also be profitable. If only the exact optimal combination works and every neighbor is a loser — that's textbook overfitting.

Visualize it as a "parameter landscape." A robust strategy has a broad hilltop — many parameter combinations that work. An overfitted strategy has a narrow spike — one combination that works, surrounded by cliffs.

Practical Anti-Overfitting Techniques

1. Keep it simple. Every additional parameter roughly doubles your risk of overfitting. The best performing live strategies I've seen use 2-4 parameters. Not 12. Not 8. Three or four.

2. Use the correct ratio of trades to parameters. You need 50-100 trades per free parameter for statistical significance. Strategy with 4 parameters? You need 200-400 trades. If your backtest period only produces 80 trades with 6 parameters, the results are statistically meaningless.

3. Test on multiple instruments. If your BTCUSDT strategy also works on ETHUSDT, SOLUSDT, and EURUSD (with appropriate adjustment), the underlying pattern is probably real. If it only works on one specific instrument during one specific time period, it's noise.

4. Walk-forward analysis. The gold standard. Walk-forward testing with rolling optimization windows is the closest thing to simulating real deployment. If your strategy passes walk-forward analysis, overfitting risk drops dramatically.

5. Out-of-sample holdout. Set aside the most recent 20-30% of your data and never touch it during development. Only run it once, at the very end. This is your final exam — no retakes allowed. If you use the out-of-sample data to "adjust" your strategy and then test again, you've contaminated it.

6. Use round numbers for parameters. RSI(14), not RSI(13.7). EMA(20), not EMA(19.3). If the edge is real, it works with standard settings. If you need fractional precision, you're fitting noise.

7. Apply Occam's Razor. Given two strategies with similar performance, choose the simpler one. It's almost always more robust. I've never seen a 10-parameter strategy outperform a 3-parameter strategy in live trading, even when the 10-parameter version looked dramatically better in backtesting.

"With four parameters I can fit an elephant, and with five I can make him wiggle his trunk." — John von Neumann. This quote from the father of computer science is the best one-sentence summary of the overfitting problem.

The Simplification Protocol

If you suspect your strategy is overfitted, here's my protocol for fixing it:

- List all parameters and filters in the strategy

- Remove the least important filter (the one that contributes least to signal quality)

- Re-run the backtest

- If performance drops less than 10%, the filter was noise — leave it out

- If performance drops more than 30%, the filter captured signal — keep it

- Repeat until you've tested every filter

I've used this process dozens of times. Almost every strategy I've simplified outperformed its complex original version in subsequent out-of-sample testing. Complexity is the enemy of robustness.

Pair this with proper backtest setup and understanding why strategies fail for a comprehensive approach to strategy development.

Build robust strategies, not overfitted ones. StratBase.ai supports parameter sensitivity testing, walk-forward analysis, and multi-instrument validation — the tools you need to keep overfitting in check.

FAQ

What is overfitting in trading?

Overfitting occurs when parameters are tuned so precisely to historical data that they capture noise rather than signal. The strategy works brilliantly on training data but fails on new data.

How many parameters is too many?

You need 50-100 trades per free parameter. 3 parameters with 300 trades is fine. 10 parameters with 100 trades is almost certainly overfitting.

Further Reading

About the Author

Trading systems developer and financial engineer. 10+ years building automated trading infrastructure and backtesting frameworks across crypto and traditional markets.

FAQ

What is overfitting in trading?▾

Overfitting occurs when a strategy's parameters are tuned so precisely to historical data that they capture noise rather than genuine market patterns. The strategy performs brilliantly on the data it was trained on but fails on new, unseen data.

How many parameters is too many for a trading strategy?▾

A useful rule of thumb: you need at least 50-100 trades per free parameter. A strategy with 5 parameters needs 250-500 trades in the testing period. If you have 3 parameters and 300 trades, you're in reasonable territory. If you have 10 parameters and 100 trades, you're almost certainly overfitting.

Further reading

Related articles

Comments (0)

Loading comments...